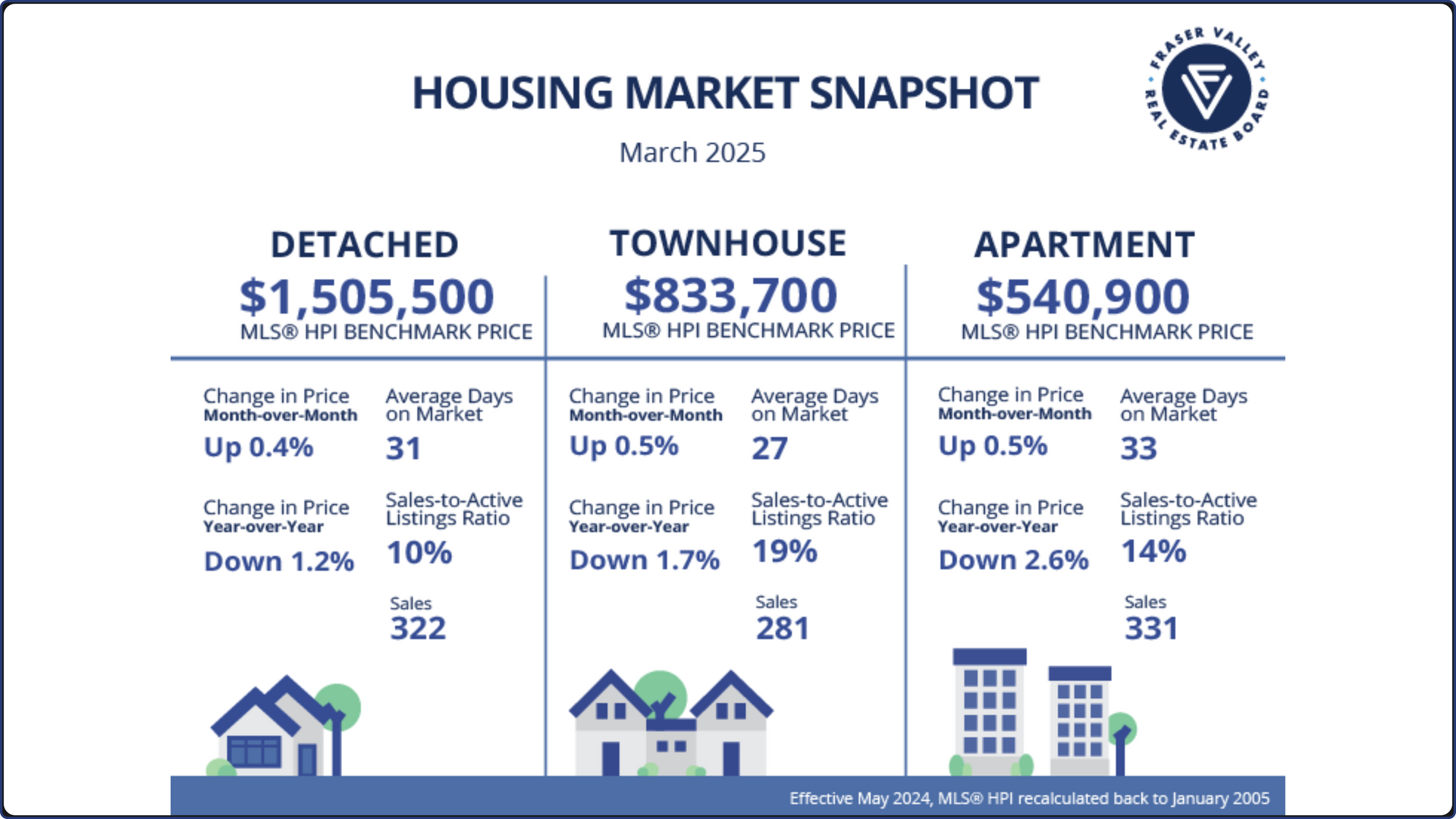

SURREY, BC – March home sales in the Fraser Valley remained nearly 50 per cent below the 10-year average — making for the slowest start to the spring market in more than 15 years. The Fraser Valley Real Estate Board recorded 1,036 sales in March, up 13 per cent from February, but still 26 per cent below sales recorded this time last year. Following a decline on the Board’s Multiple Listing Service® (MLS®) in February, new listings increased 22 per cent in March to 3,800. Overall inventory is at a decade-high level, with 9,219 active listings, 49 per cent above March 2024 and 59 per cent above the 10-year seasonal average.

For a short time, parks and streets in Surrey, White Rock and Delta will soon be filled with the white and pink hues of cherry blossoms. Those beautiful blooms are around for only a couple of weeks every April. This week, Discover Surrey posted a list of favourite places to see the Japanese flowering trees in Surrey, including Bear Creek Park (13750 88 Ave.), Nico-Wynd Golf Course (3601 Nico-Wynd Place), 95 Avenue at 154 Street, Spenser Drive at 151A Street and 150B Street at 24 Avenue. Find out more.

Under normal circumstances — anyone remember what those feel like? — falling mortgage rates would be fuel for the spring housing market. But it’s hard to start a fire when the Canadian economy is soaked through with tariff-related fear and uncertainty. The Bank of Canada is doing what it can to warm home buyers up. By lowering the overnight rate for the seventh consecutive time today, the Bank has helped slash 2.25% from variable mortgage rates since June 2024. Once lenders absorb today’s cut, both five-year variable rates and the most common fixed rates will be available for below 4%. Historically, those are approachable rates. But we’ll soon find out how little rates matter when home buyers face an unprecedented threat to their livelihoods. Read More