Baby eagles seemed appropriate after the Superbowl result. Would have much preferred it to be putting a baby Bengal Tiger but maybe next year! Support our very own LAPS 📣 "He is not a full man who does not own a piece of land." — Hebrew Proverb

The Township of Langley Traffic Cameras for up to date traffic information. Click here

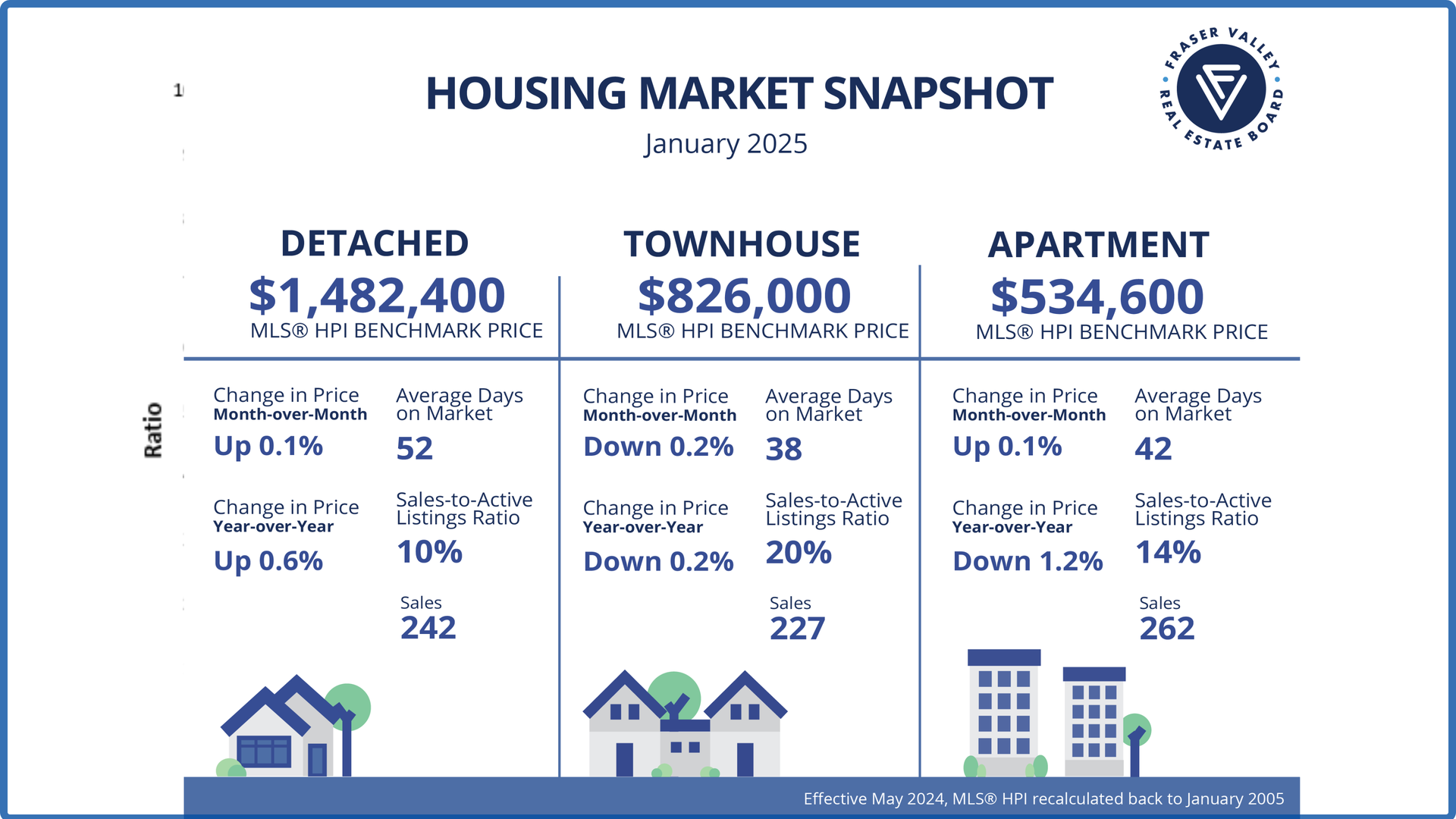

SURREY, BC — Growing inventory and stable prices could lead to opportunities for buyers in the Fraser Valley market this winter despite uncertain economic conditions. Read More